Title loans can be a valuable resource for individuals in need of fast cash without alternative options.

What if, on a Monday morning, as you rush out the door, your car decides it’s time to take a nap? You’re left with a hefty repair bill and no way to get to work.

According to a recent survey, nearly 60% of Americans have faced unexpected expenses in the past year, often with no savings to cover the cost. You might happen to be a victim of such a crisis or someone looking for some help in such situations. This read is for you.

Title loans – a potential lifesaver for those who need quick cash and have nowhere else to turn. But what exactly is a title loan, and why might it be the right choice for your financial emergency?

Hold on to your horns while we take you on a ride about title loans, examining how they work, their benefits and drawbacks, and if they might be the answer you’re looking for.

What are Title Loans?

A title loan is a type of secured loan where your vehicle’s title is used as collateral. This means you borrow money against the value of your car. If you own your car outright or have significant equity in it, you can use its title to secure a loan.

Title loans are typically made to borrowers with lower incomes or poor credit ratings. These borrowers are often unable to obtain other forms of financing, such as a personal line of credit. Due to the higher risk of default, title loans generally carry high interest rates.

Critics argue that vehicle title loans are a form of predatory lending because title lending exploits desperate borrowers who lack apparent alternatives. Defenders of the practice argue that title lending is entitled to higher interest rates and collateral due to the higher-than-average default risk associated with vehicle title loans.

How Do Title Loans Work?

The first step to obtaining a title loan is to have your vehicle evaluated by the title lender. They will assess its market value based on factors like make, model, year, mileage, and condition. Once the vehicle’s value is determined and other title loan requirements are met, you can apply. This process typically requires providing your vehicle title, a photo ID, and sometimes proof of income.

If approved, the lender presents the loan terms, including the amount, interest rate, fees, and repayment schedule. It’s crucial to understand and agree to these terms before proceeding.

Once the terms are agreed upon, you receive the loan amount, often on the same day. This quick access to cash is one of the main benefits of vehicle title loans.

Repayment is the final step. You must repay the loan in full by the end of the term, including the principal amount, interest, and any applicable fees. Failure to repay can result in the lender repossessing your vehicle.

Pros and Cons of Title Loans

Title loans can be both a blessing and a curse, depending on your situation and how you manage the loan.

One of the main advantages of title loans is the speed of access to cash. If you’re in a financial bind and need money quickly, title loans can provide funds within a day, sometimes even within hours. Additionally, since vehicle title loans are secured with your vehicle, they typically do not require a credit check. This makes them accessible to those with poor or no credit history

However, the downsides are significant. Title loans come with very high interest rates, which can lead to a cycle of debt if you’re unable to repay the loan quickly. The short repayment terms, often just 15 to 30 days, add to this risk.

The most severe consequence of failing to repay a title loan is the loss of your vehicle, as the lender has the right to repossess it. This can be devastating if your car is your primary mode of transportation.

How to Choose a Title Loan Lender

Choosing the right lender is crucial to ensure you get the best terms and avoid falling into predatory lending traps. Start by researching various lenders and reading reviews from other borrowers. Websites like the Better Business Bureau can provide valuable insights into a lender’s reputation.

When evaluating title lending providers, pay close attention to the interest rates they offer. Title loans inherently come with high interest rates, but some lenders charge exorbitantly more than others. Make sure to ask for a detailed breakdown of all fees, including any hidden charges that might not be immediately noticeable.

Another critical aspect is the repayment terms. While vehicle title loans typically have short repayment periods, some lenders may offer more flexibility than others. Ensure that the repayment schedule is manageable within your financial situation to avoid defaulting on the loan.

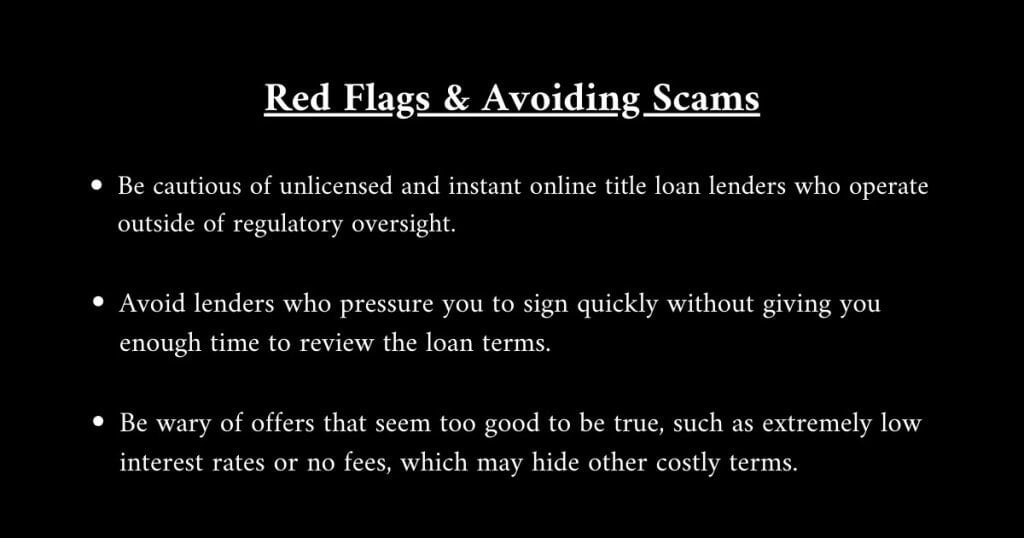

It’s also essential to be aware of red flags that might indicate predatory instant online title loan lenders. Be cautious of lenders who pressure you to sign quickly without giving you enough time to review the loan terms.

Unlicensed lenders or some instant online title loan providers are another significant risk. They operate outside of regulatory oversight and are more likely to engage in unethical practices. Always verify that the lender is licensed to operate in your state.

Legal and Regulatory Considerations

Understanding the legal fine print of title loans can help you make informed decisions and protect yourself from predatory practices.

Here’s what you need to know:

State Regulations for Title Lending

Title loan regulations vary significantly by state. Some states have strict regulations, while others have none, affecting the terms and legality of Vehicle title loans. Interest rate caps and minimum and maximum loan terms are standard regulatory measures to protect borrowers.

Borrower Rights

Lenders are required to disclose all loan terms, including the total cost of the loan, interest rate, and any fees. Know your rights regarding vehicle repossession. Some states have laws that provide a grace period or require lenders to provide notice before repossessing your vehicle. If you feel you’ve been treated unfairly, you can file a complaint with your state’s attorney general or consumer protection agency.

Federal Regulations

The Truth in Lending Act (TILA) requires lenders to disclose the terms and cost of the loan, ensuring you understand the full financial impact before agreeing to the loan. The Fair Debt Collection Practices Act (FDCPA) protects you from abusive or unfair debt collection practices if you default on your loan.

Title Loans vs. Registration Loans

When it comes to borrowing money using your vehicle as collateral, you have two main options: title loans and registration loans. While they may seem similar, they have distinct differences that can significantly impact your decision.

Let’s break them down.

Title loans use your vehicle title as collateral, meaning the lender can repossess your car if you fail to repay the loan. You can borrow a higher amount, usually 25% to 50% of your vehicle’s value, but they come with high interest rates and short repayment terms, typically between 15 to 30 days.

On the other hand, registration loans use your vehicle registration as collateral. You do not need to own your car outright, making it accessible even if you’re still making payments on it. The lender places a lien on the registration, not the title. The loan amount for registration loans is generally lower, as it depends on the lender’s assessment of your ability to repay rather than the full value of the vehicle.

While the risk of repossession is present, depending on state laws, it may not be as immediate or direct as with title loans. Registration loans also come with high interest rates, sometimes slightly lower than title loans, and similarly short repayment terms.

Title loans are best for those who own their vehicle outright and need a larger loan amount quickly, while registration loans are suitable for individuals who are still making car payments and need a smaller, quick loan.

Our take on the Title Loans

While title loans can offer immediate relief, they should be approached with caution and used only when you have a clear repayment plan. Always research the best title loan companies around you thoroughly, be aware of your rights, and avoid predatory practices to ensure your financial well-being.

Stay tuned for more tips and advice to help you manage your finances wisely and effectively.